Macroeconomic Headwinds and the Indian Rupee

The Indian Rupee has faced significant downward pressure over the last year, depreciating by approximately 11% against the US Dollar. This slide is driven by a combination of a strengthening greenback, sustained foreign institutional investor (FII) outflows, and a widening trade deficit. While a weaker Rupee can benefit exporters, the immediate concern for the economy is the rising cost of essential imports like crude oil, electronics, and fertilizers.

The Reserve Bank of India has been active in the foreign exchange market, using its massive reserves to curb extreme volatility and ensure an orderly depreciation. However, the global ‘interest rate differential’ remains a major hurdle. With the US Fed maintaining high rates, capital continues to flow back to safer US assets, leaving emerging market currencies vulnerable. For businesses with significant dollar-denominated debt, the 11% slide is a major stress test for their balance sheets.

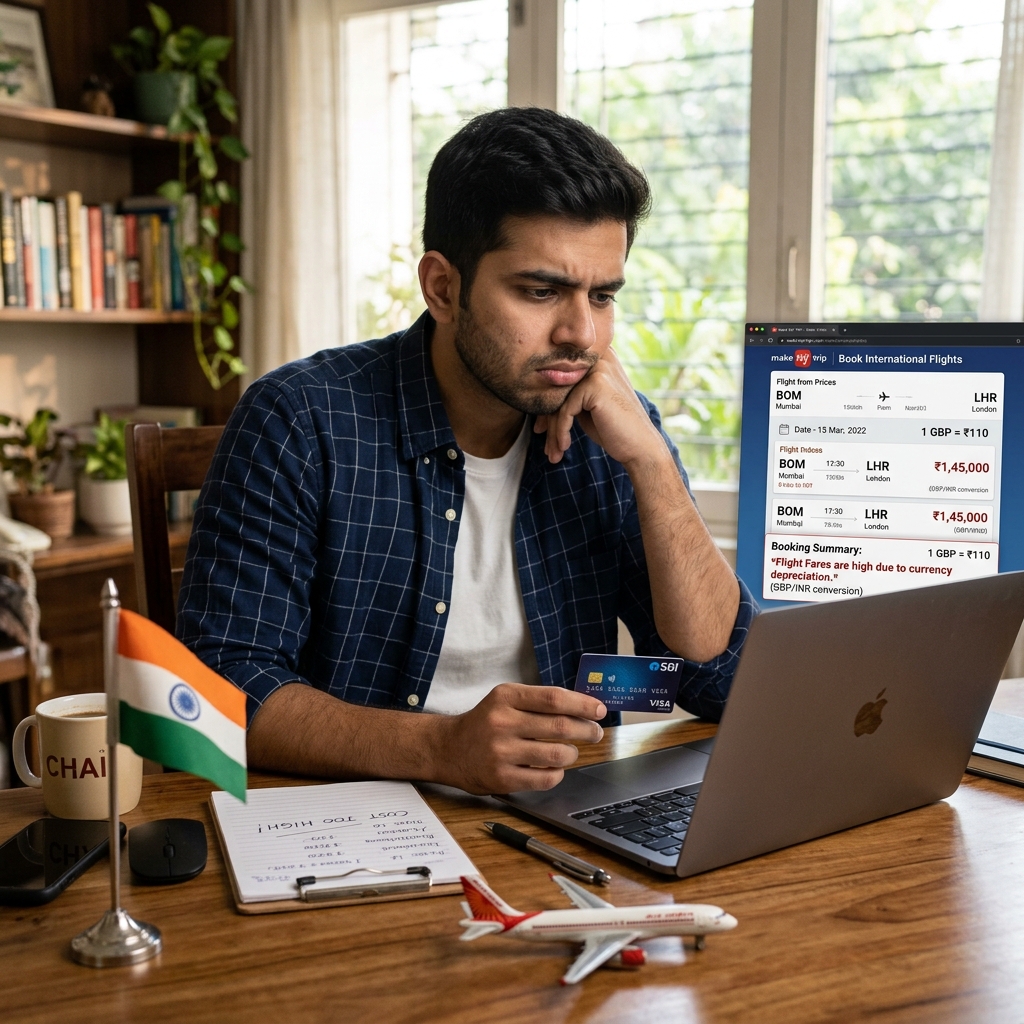

On the ground, consumers are feeling the pinch through ‘imported inflation’. Electronics, high-end cars, and foreign travel have become noticeably more expensive. To mitigate the impact, the government is focusing on ‘Rupee Trade’ agreements with partner nations to settle imports in local currency. The path ahead for the Rupee will depend heavily on the global oil price trajectory and the pace of rate cuts by the US Federal Reserve.